But price inelasticity of demand is just one reason why trying to provide services like healthcare through the private sector can be problematic. An even bigger one is the problem of asymmetric information – where the seller knows more information relevant to the transaction than the buyer does, or vice-versa. In the case of healthcare, this can be something as basic as patients not fully understanding all the arcane details of which medical services they should accept and how those services will be charged and how much their insurance will actually cover and so on – which, in many cases, can screw them over hard when it turns out that they weren’t as covered as they thought they were. As Aaron Carroll notes:

Most people don’t find out that they’re not getting “good service” [on their health insurance] until they’re sick. Healthy people don’t make much use of their insurance, so they don’t know how bad it is. They only find out after they’re ill, and then it’s too late.

But patients aren’t the only ones who have to deal with information asymmetries; their doctors and insurance providers often face equally daunting information problems themselves. In fact, the problem of information asymmetry pervades practically every aspect of the healthcare sector – and a number of other sectors as well. Wheelan provides a full rundown:

Information matters, particularly when we don’t have all that we need. Markets tend to favor the party that knows more. (Have you ever bought a used car?) But if the imbalance, or asymmetry of information, becomes too large, then markets can break down entirely. This was the fundamental insight of 2001 Nobel laureate George Akerlof, an economist at the University of California, Berkeley. His paper entitled “The Market for Lemons” used the used-car market to make its central point. Any individual selling a used car knows more about its quality than someone looking to buy it. This creates an adverse selection problem. […] Car owners who are happy with their vehicles are less likely to sell them. Thus, used-car buyers anticipate hidden problems and demand a discount. But once there is a discount built into the market, owners of high-quality cars become even less likely to sell them—which guarantees the market will be full of lemons. In theory, the market for high-quality used cars will not work, much to the detriment of anyone who may want to buy or sell such a car. (In practice, such markets often do work for reasons explained by the gentlemen with whom Mr. Akerlof shared his Nobel prize; more on that in a moment.)

“The Market for Lemons” is characteristic of the kinds of ideas recognized by the Nobel committee. It is, in the words of the Royal Swedish Academy of Sciences, “a simple but profound and universal idea, with numerous implications and widespread applications.” Health care, for example, is plagued with information problems. Consumers of health care—the patients—almost always have less information about their care than their doctors do. Indeed, even after we see a doctor, we may not know whether we were treated properly. This asymmetry of information is at the heart of our health care woes.

Under any “fee for service” system, doctors charge a fee for each procedure they perform. Patients do not pay for these extra tests and procedures; their insurance companies (or the federal government, in the case of older Americans who are eligible for Medicare) do. At the same time, medical technology continues to present all kinds of new medical options, many of which are fabulously expensive. This combination is at the heart of rapidly rising medical costs: Doctors have an incentive to perform expensive medical procedures and patients have no reason to disagree. If you walk into your doctor’s office with a headache and the doctor suggests a CAT scan, you would almost certainly agree “just to be sure.” Neither you nor your doctor is acting unethically. When cost is not a factor, it makes perfect sense to rule out brain cancer even when the only symptom is a headache the morning after the holiday office party. Your doctor might also reasonably fear that if she doesn’t order a CAT scan, you might sue for big bucks later if something turns out to be wrong with your head.

Medical innovation is terrific in some cases and wasteful in others. Consider the current range of treatments for prostate cancer, a cancer that afflicts many older men. One treatment option is “watchful waiting,” which involves doing nothing unless and until tests show that the cancer is getting worse. This is a reasonable course of action because prostate cancer is so slow-growing that most men die of something else before the prostate cancer becomes a serious problem. Another treatment option is proton radiation therapy, which involves shooting atomic particles at the cancer using a proton accelerator that is roughly the size of a football field. Doing nothing essentially costs nothing (more or less); shooting protons from an accelerator costs somewhere in the range of $100,000.

The cost difference is not surprising; the shocking thing is that proton therapy has not been proven any more effective than watchful waiting. An analysis by the RAND Corporation concluded, “No therapy has been shown superior to another.”

Health maintenance organizations were designed to control costs by changing the incentives. Under many HMO plans, general practitioners are paid a fixed fee per patient per year, regardless of what services they provide. Doctors may be restricted in the kinds of tests and services they can prescribe and may even be paid a bonus if they refrain from sending their patients to see specialists. That changes things. Now when you walk into the doctor’s office (still at a disadvantage in terms of information about your own health) and say, “I’m dizzy, my head hurts, and I’m bleeding out my ear,” the doctor consults the HMO treatment guidelines and tells you to take two aspirin. As exaggerated as that example may be, the basic point is valid: The person who knows most about your medical condition may have an economic incentive to deny you care. Complaints about too much spending are replaced by complaints about too little spending. Every HMO customer has a horror story about wrangling with bureaucrats over acceptable expenses. In the most extreme (and anecdotal) stories, patients are denied lifesaving treatments by HMO bean counters.

Some doctors are willing to do battle with the insurance companies on behalf of their patients. Others simply break the rules by disguising treatments that are not covered by insurance as treatments that are. (Patients aren’t the only ones suffering from an asymmetry of information.) Politicians have jumped into the fray, too, demanding things like disclosure of the incentives paid to doctors by insurance companies and even a patient’s bill of rights.

The information problem at the heart of health care has not gone away: (1) The patient, who does not pay the bill, demands as much care as possible; (2) the doctor maximizes income and minimizes lawsuits by delivering as much care as possible; (3) the insurance company maximizes profits by paying for as little care as possible; (4) technology has introduced an array of massively expensive options, some of which are miracles and others of which are a waste of money; and (5) it is very costly for either the patient or the insurance company to prove the “right” course of treatment. In short, information makes health care different from the rest of the economy. When you walk into an electronics store to buy a big-screen TV, you can observe which picture looks clearest. You then compare price tags, knowing that the bill will arrive at your house eventually. In the end, you weigh the benefits of assorted televisions (whose quality you can observe) against the costs (that you will have to pay) and you pick one. Brain surgery really is different.

The fundamental challenge of health care reform is paying for the “right” treatment—the “product” that makes the most sense relative to what it costs. This is an exercise that consumers perform on their own everywhere else in the economy. Bean counters should not automatically say no to super-expensive treatments; some may be wonderfully effective and worth every penny. They should say no to expensive treatments that are not demonstrably better than less expensive options. They should also say no to doing some tests “just to be sure,” both because these diagnostics are expensive, but also because when administered to healthy people they tend to generate “false positives,” which can breed expensive, unnecessary, and potentially dangerous follow-up care.

There is an old aphorism in advertising: “I know I’m wasting half my money; I just wish I knew which half.” Health care is similar, and if the goal of health care reform is to restrain rapidly rising costs, then any policy change will have to focus on quality and outcomes rather than just paying for inputs. New York Times financial columnist David Leonhardt describes the treatment for prostate cancer (where fabulously expensive technology does not appear to be delivering better health) as his own “personal litmus test” for health care reform. He writes, “The prostate cancer test will determine whether President Obama and Congress put together a bill that begins to fix the fundamental problem with our medical system: the combination of soaring costs and mediocre results. If they don’t, the medical system will remain deeply troubled, no matter what other improvements they make.”

—

But we’re not done with health care yet. The doctor may know more about your health than you do, but you know more about your long-term health than your insurance company does. You may not be able to diagnose rare diseases, but you know whether or not you lead a healthy lifestyle, if certain diseases run in your family, if you are engaging in risky sexual behavior, if you are likely to become pregnant, etc. This information advantage has the potential to wreak havoc on the insurance market.

Insurance is about getting the numbers right. Some individuals require virtually no health care. Others may have chronic diseases that require hundreds of thousands of dollars of treatment. The insurance company makes a profit by determining the average cost of treatment for all of its policyholders and then charging slightly more. When Aetna writes a group policy for 20,000 fifty-year-old men, and the average cost of health care for a fifty-year-old man is $1,250 a year, then presumably the company can set the annual premium at $1,300 and make $50—on average—for each policy underwritten. Aetna will make money on some policies and lose money on others, but overall the company will come out ahead—if the numbers are right.

Is this example starting to look like […] the used-car market? It should. The $1,300 policy is a bad deal for the healthiest fifty-year-old men and a very good deal for the overweight smokers with a family history of heart disease. So, the healthiest men are most likely to opt out of the program; the sickest guys are most likely to opt in. As that happens, the population of men on which the original premium was based begins to change; on average, the remaining men are less healthy. The insurance company studies its new pool of middle-aged men and reckons that the annual premium must be raised to $1,800 in order to make a profit. Do you see where this is going? At the new price, more men—the most healthy of the unhealthy—decide that the policy is a bad deal, so they opt out. The sickest guys cling to their policies as tightly as their disease-addled bodies will allow. Once again the pool changes and now even $1,800 does not cover the cost of insuring the men who sign up for the program. In theory, this adverse selection could go on until the market for health insurance fails entirely.

That does not actually happen. Insurance companies usually insure large groups whose individuals are not allowed to select in or out. If Aetna writes policies for all General Motors employees, for example, then there will be no adverse selection. The policy comes with the job, and all workers, healthy and unhealthy, are covered. They have no choice. Aetna can calculate the average cost of care for this large pool of men and women and then charge a premium sufficient to make a profit.

Writing policies for individuals, however, is a much scarier undertaking. Companies rightfully fear that the people who have the most demand for health coverage (or life insurance) are those who need it most. This will be true no matter how much an insurance company charges for its policies. At any given price—even $5,000 a month—the individuals who expect their medical costs to be higher than the cost of the policy will be the most likely to sign up. Of course, the insurance companies have some tricks of their own, such as refusing coverage to individuals who are sick or likely to become sick in the future. This is often viewed as some kind of cruel and unfair practice perpetrated on the public by the insurance industry. On a superficial level, it does seem perverse that sick people have the most trouble getting health insurance. But imagine if insurance companies did not have that legal privilege. A (highly contrived) conversation with your doctor might go something like this:

DOCTOR: I’m afraid I have bad news. Four of your coronary arteries are fully or partially blocked. I would recommend open-heart surgery as soon as possible.

PATIENT: Is it likely to be successful?

DOCTOR: Yes, we have excellent outcomes.

PATIENT: Is the operation expensive?

DOCTOR: Of course it’s expensive. We’re talking about open-heart surgery.

PATIENT: Then I should probably buy some health insurance first.

DOCTOR: Yes, that would be a very good idea.

Insurance companies ask applicants questions about family history, health habits, smoking, dangerous hobbies, and all kinds of other personal things. When I applied for term life insurance, a representative from the company came to my house and drew blood to make sure that I was not HIV-positive. He asked whether my parents were alive, if I scuba dive, if I race cars. (Yes, yes, no.) I peed in a cup; I got on a scale; I answered questions about tobacco and illicit drug use—all of which seemed reasonable given that the company was making a commitment to pay my wife a large sum of money should I die in the near future.

Insurance companies have another subtle tool. They can design policies, or “screening” mechanisms, that elicit information from their potential customers. This insight, which is applicable to all kinds of other markets, earned Joseph Stiglitz, an economist at Columbia University and a former chief economist of the World Bank, a share of the 2001 Nobel Prize. How do firms screen customers in the insurance business? They use a deductible. Customers who consider themselves likely to stay healthy will sign up for policies that have a high deductible. In exchange, they are offered cheaper premiums. Customers who privately know that they are likely to have costly bills will avoid the deductible and pay a higher premium as a result. (The same thing is true when you are shopping for car insurance and you have a sneaking suspicion that your sixteen-year-old son is an even worse driver than most sixteen-year-olds.) In short, the deductible is a tool for teasing out private information; it forces customers to sort themselves.

—

Any insurance question ultimately begs one explosive question: How much information is too much? I guarantee that this will become one of the most nettlesome policy problems in coming years. Here is a simple exercise. Pluck one hair from your head. (If you are totally bald, take a swab of saliva from your cheek.) That sample contains your entire genetic code. In the right hands (or the wrong hands), it can be used to determine if you are predisposed to heart disease, certain kinds of cancer, depression, and—if the science continues at its current blistering pace—all kinds of other diseases. With one strand of your hair, a researcher (or insurance company) may soon be able to determine if you are at risk for Alzheimer’s disease—twenty-five years before the onset of the disease. This creates a dilemma. If genetic information is shared widely with insurance companies, then it will become difficult, if not impossible, for those most prone to illness to get any kind of coverage. In other words, the people who need health insurance most will be the least likely to get it—not just the night before surgery, but ever. Individuals with a family history of Huntington’s disease, a hereditary degenerative brain disorder that causes premature death, are already finding it hard or impossible to get life insurance. On the other hand, new laws are forbidding insurance companies from gathering such information, leaving them vulnerable to serious adverse selection. Individuals who know that they are at high risk of getting sick in the future will be the ones who load up on generous insurance policies.

An editorial in The Economist noted this looming quandary: “Governments thus face a choice between banning the use of test results and destroying the industry, or allowing their use and creating an underclass of people who are either uninsurable or cannot afford to insure themselves.” The Economist, which is hardly a bastion of left-wing thought, suggested that the private health insurance market may eventually find this problem intractable, leaving government with a much larger role to play. The editorial concluded: “Indeed, genetic testing may become the most potent argument for state-financed universal health care.”

Any health care reform that seeks to make health insurance both more accessible and more affordable, particularly for those who are sick or likely to get sick, will have devastating adverse selection problems. Think about it: If I promise that you can buy affordable insurance, regardless of whether or not you are already sick, then the optimal time to buy that insurance is in the ambulance on the way to the hospital. The only fix for this inherent problem is to combine guaranteed access to affordable insurance with a requirement that everyone buy insurance—healthy and sick, young and old—a so-called “personal mandate.” The insurance companies will still lose money on the policies that they are forced to sell to bad risks, but those losses can be offset by the profits earned from healthy people who are forced to buy insurance. (Any country with a national health care system effectively has a personal mandate; all citizens are forced to pay taxes, and in return they all get government-funded health care.)

This is the approach that Massachusetts took as part of a state plan to provide universal access to health insurance. State residents who can afford health insurance but don’t buy it are fined on their state tax return. Hillary Clinton supported a personal mandate in the 2008 Democratic presidential primaries; Barack Obama did not, though that arguably had more to do with distinguishing himself from his toughest Democratic opponent than it did with his analysis of adverse selection. Obviously, forcing healthy people to buy something that they would otherwise not buy is a heavy-handed use of government; it’s also the only way to pool risk (which is the purpose of insurance) when the distribution of risk is not random.

Here are the relevant economics: (1) We know who is sick; (2) increasingly we know who will become sick; (3) sick people can be extremely expensive; and (4) private insurance doesn’t work well under these circumstances. That’s all straightforward. The tough part is philosophical/ideological: To what extent do we want to share health care expenses anyway (if at all), and how should we do it? Those were the fundamental questions when Bill Clinton sought to overhaul health care in 1993, and again when the Obama administration took it up in 2009.

Shortly after Wheelan wrote this, of course, the Obama administration did in fact pass a healthcare plan that included a personal mandate for every citizen to get health insurance, along with a rule that insurance companies could no longer deny coverage to people with pre-existing conditions. In practice, though, actually enforcing this policy has proven difficult – it’s hard to force people to buy something if their whole problem is that they don’t feel they can afford it – so millions of Americans still remain uninsured today.

The alternative to this kind of patchwork approach is universal coverage – a policy of just having one big insurance pool that includes everyone in the country. Having a large insurance pool means that each individual member of that pool becomes cheaper to insure – so naturally, having an insurance pool that encompasses everyone will be cheapest of all. Every advanced industrial country except the US has figured this out and adopted some form of universal health insurance, and they’ve enjoyed massive savings on their healthcare as a result – but meanwhile, the US still continues to waste billions of dollars on its inefficient privatized system that doesn’t even cover everybody. As Taylor writes:

[One] thing insurance companies can do to mitigate risk is to draw upon a larger pool of customers. The larger the customer pool, the more likely it is to contain a good percentage of low-risk participants to offset the high-risk ones. Thus, health insurance can be less expensive if purchased through your employer than for you as an individual, and health insurance is often less expensive per person for a large company than a small one. In the car insurance market, almost every state requires every car owner to get insurance, so low-risk drivers can’t drop out of the market, which again moderates the whole pool’s risk.

In most of the industrialized world, the imperfect information problems inherent to the health insurance market have been addressed by a nationalized health care system. Countries have structured their national programs in a variety of ways, but they share a belief that the problem of imperfect information is so great in health care that a free market cannot cope with it. Governments around the world—except in the United States—address the [problem of potential over-treatment] by controlling the amount of care provided, when care should be delivered, and how much it should cost. They address the adverse selection problem by bringing the whole country into the insurance pool.

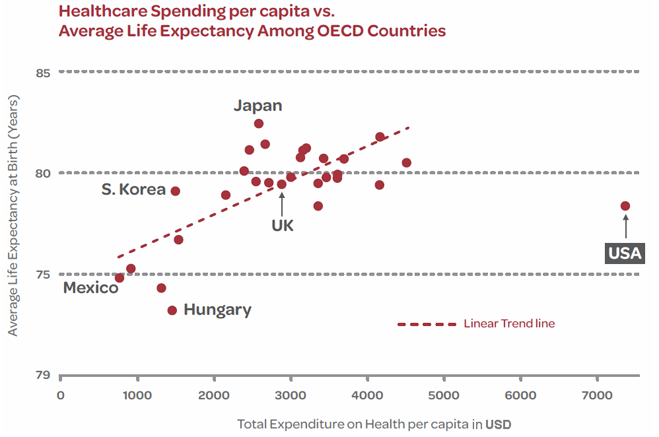

As you may know, the United States spends much more on health care than any industrialized nation in the world. According to the World Health Organization, in 2007 U.S. health care spending (both privately and publicly funded) was about $7,300 per person. In comparison, Canada, France, Germany, Japan, and the United Kingdom spent between $2,700 and $3,900 per person. As a share of gross domestic product, health care spending in the United States was 15.7 percent; in Canada, France, and Germany it was between 10 and 11 percent of GDP; and in Japan and the United Kingdom it was roughly 8 percent of GDP. In short, the United States is spending twice as much per person on health care as do other nations with comparable economies.

A standard explanation for this pattern is the extraordinary quality of both health care and health care research in the United States. Innovation—whether in pharmaceuticals or equipment—is better rewarded, and doctors and nurses are better compensated for their hard work and long years of schooling. Yet it doesn’t appear that the quality of U.S. health care is twice as good as in these other nations. The United States doesn’t seem to be seeing a big enough payoff in terms of health for this high level of spending, especially given that through the mid-2000s, 40 million people in the country had no health insurance at all.

Despite the US being the only holdout in this area, American conservatives still have strong objections to the idea of getting government more involved in the provision of healthcare. But as Alexander demonstrates, their objections all have straightforward responses:

[Q]: Government would do a terrible job in health care. We should avoid government-run “socialized” medicine unless we want cost overruns, long waiting times, and death panels.

Government-run health systems empirically do better than private health systems, while also costing much less money.

Let’s compare, for example, Sweden, France, Canada, the United Kingdom, and the United States. The first four all have single-payer health care (a version of government-run health system); the last has a mostly private health system (although it shouldn’t matter, we’ll use statistics from before Obamacare took effect). We’ll look at three representative statistics commonly used to measure quality of health care: infant mortality, life expectancy, and cancer death rate.

Infant mortality is the percent of babies who die in the first few weeks of life, usually a good measure of pediatric and neonatal care. Of the five countries, Sweden has the lowest infant mortality at 2.56 per 1,000 births, followed by France at 3.54, followed by the UK at 4.91, followed by Canada at 5.22, with the United States last at 6.81. (source)

Life expectancy, the average age a person born today can expect to live, is a good measurement of lifelong and geriatric care. Here Sweden is again first at 80.9, France and Canada tied for second at 80.7, the UK next at 79.4, and the United States once again last at 78.3. (source)

Taking cancer deaths per 100,000 people per year as representative of deaths from serious disease, here we find the UK doing best at 253.5 deaths, Sweden second at 268.2, France in third at 286.1, and the United States again in last place at 321.9 deaths (source: OECD statistics; data for Canada not available).

So we notice that the United States does worse than all four countries with single-payer health systems, even though America is wealthier per capita than any of them. This is not statistical cherry-picking: any way you look at it, the United States has one of the least effective health systems in the developed world.

[Q]: Government-run health care would be bloated, bureaucratic, and unnecessarily expensive, as opposed to the sleek, efficient service we get from the free market.

Actually, government-run health care is empirically more efficient than market health care. For example, Blue Cross New England employs more people to administer health insurance for its 2.5 million customers than the Canadian health system employs to administer health insurance for 27 million Canadians. Health care spending per person (public + private) in Canada is half what it is in America, yet Canadians have longer life expectancy, lower infant mortality, and are healthier by every objective standard.

Remember those five countries from the last question?

The UK spends $1,675 per person per year on health care. Canada spends $1,939. Sweden, which you’ll remember did best on most of the statistics, spends $2,125. France spends $2,288. Americans spend on average $4,271 – almost three times as much as Britain, a country which delivers better health care.

When this argument gets put in graph form, it becomes even clearer that US health inefficiency is literally off the chart.

If these were companies in the free market, the company that charges three times as much to provide a worse service would have gone bankrupt long ago. That company is American-style private health care.

[Q]: In government-run health care, people are relegated to “waiting lists”, where they have to wait months or even years for doctor visits, surgeries, and other procedures. Sometimes people die on these waiting lists. Obviously, this is unacceptable and a knock-down argument against government-run health care.

The laws of supply and demand apply in health care as much as anywhere else: people would like to see doctors as quickly as possible, but doctors are a scarce resource that must be allocated somehow.

In a private system, doctor access is allocated based on money; this has the advantage of incentivizing the production of more doctors and of ensuring that people with enough money can see doctors quickly. These are also its disadvantages: assuming more people want to see a doctor than need to do so, costs will spiral out of control and poor people will have limited or no access.

In a public system, doctor access is allocated based on medical need. Although no one will be turned away from a doctor in an emergency situation, people may have to wait a long amount of time for elective surgeries in order that other sicker people, including poor people who would not be seen at all in a private system, can be seen first.

The relative effectiveness of the two systems can once again be seen in the infant mortality, life expectancy, and cancer survival rate statistics.

[Q]: Government-run health care inevitably includes “death panels” who kill off expensive patients in order to save money on health care costs.

The private system as it exists now in America also has bodies that make these kinds of rationing decisions. Health care rationing is not some sinister conspiracy but a reasonable response to limited resources. The complete argument is here, but I can sum up the basics:

Insurance providers, whether they are a government agency or a private corporation, have a finite amount of money; they can only spend money they have. In one insurance company, customers might pay hundred million dollars in fees each year, so the total amount of money the insurance company can spend on all its customers that year is a hundred million dollars. In reality, since it is a business, it wants to make a profit. Let’s say it wants a profit of ten percent. That means the total amount of money it has to spend is ninety million dollars.

But as a simplified example, let’s reduce this to an insurance company with one hundred customers, each of whom pays $1. This insurance company wants 10% profit, so it has $90 to spend (instead of our real company’s $90 million). Seven people on the company’s plan are sick, with seven different diseases, each of which is fatal. Each disease has a cure. The cures cost, in order, $90, $50, $40, $20, $15, $10, and $5.

We are far too nice to ration health care with death panels; therefore, we have decided to give everyone every possible treatment. So when the first person, the one with the $90 disease, comes to us, we gladly spend $90 on their treatment; it would be inhuman to just turn them away. Now we have no money left for anyone else. Six out of seven people die.

The fault here isn’t with the insurance company wanting to make a profit. Even if the insurance company gave up its ten percent profit, it would only have $10 more; enough to save the person with the $10 disease, but five out of seven would still die.

A better tactic would be to turn down the person with the $90 disease. Instead, treat the people with $5, $10, $15, $20, and $40 diseases. You still use only $90, but only two out of seven die. By refusing treatment to the $90 case, you save four lives. This solution can be described as more cost-effective; by spending the same amount of money, you save more people. Even though “cost-effectiveness” is derided in the media as being opposed to the goal of saving lives, it’s actually all about saving lives.

If you don’t know how many people will get sick next year with what diseases, but you assume it will be pretty close to the amount of people who get sick this year, you might make a rule for next year: Treat everyone with diseases that cost $40 or less, but refuse treatment to anyone with diseases that cost $50 or more.

This rule remains true in the case of the $90 million insurance company. In their case, no one patient can use up all the money, but they still run the risk of spending money in a way that is not cost-effective, causing many people to die. Like the small insurance company, they can increase cost-effectiveness by creating a rule that they won’t treat people with diseases that cost more than a certain amount.

So, as one commentator pointed out, “death panels” should be called “life panels”: they aim to maximize the total number of lives that can be saved with a certain limited amount of resources.

[Q]: Why is government-run health care so much more effective?

A lot of it is economies of scale: if the government is ensuring the entire population of a country, it can get much better deals than a couple of small insurance companies. But a lot of it is more complicated, and involves people’s status as irrational consumers of health products. A person sick with cancer doesn’t want to hear a cost-benefit analysis suggesting that the latest cancer treatment is probably not effective. He wants that treatment right now, and the most successful insurance companies and hospitals are the ones that will give it to him. Here’s a good article explaining some of the systematic flaws in the economics of health care under the American system.

It could also be that really good health care and the profit motive don’t mix: studies show that for-profit hospitals are more expensive, and have poorer care (as measured in death rates) than not-for-profit hospitals.

There are all kinds of other factors that we could get into as well (and it’s a big enough topic that it could potentially comprise a whole separate post of its own one day). The simplest takeaway here, though, is that there are some goods that are simply more efficient to pay for as a collective than as separate individuals. This is true for health insurance, for all the reasons we’ve been discussing; but for similar reasons, it’s also true for other goods, like, say, insurance against the potentially-debilitating effects of old age – i.e. Social Security. Heath provides perhaps the best summary of the dynamic as a whole, and how it can apply to all different kinds of goods and services:

Despite the agreeable homophony between “public good” and “public sector,” most of what governments are in the business of providing is not public goods, but rather what economists call club goods. This term was introduced by the economist James M. Buchanan to bridge what he described as “the awesome Samuelson gap between the purely private and the purely public good.” Every good, Buchanan pointed out, has what might be referred to as an “optimal sharing group.” Your toothbrush, for instance, probably has an optimal sharing group of one, making it a good candidate for treatment as a purely private good. But other things are not like this. For instance, it’s not a great idea to spend too much money on exercise equipment. While it is convenient to have an elliptical trainer in the basement so you can work out in the privacy of your own home, this very expensive piece of equipment is likely to sit unused 362 days of the year. If your neighbor has an equally unused StairMaster, and someone else a stationary bike, then there are obvious efficiency gains to be had from sharing exercise equipment. One could organize a complicated rotation scheme among neighbors, or one could do what most people do, which is simply to take out a gym membership.

A “gym” is basically an arrangement through which individuals collectively purchase and share a variety of different types of fitness equipment. Such an arrangement is advantageous because use of this equipment is relatively nonrival. The equipment is quite durable, and so is not noticeably eroded in the short term through multiple use. Furthermore, the amount of time that any one person wants to spend using it represents a relatively small fraction of the day, which makes it well suited for sharing. Thus the way that we typically organize consumption is by charging people a flat fee for access to the club, which then gives them “free” access to all the machines within.

There are a couple of things worth noting about this arrangement. The first is that the use of a flat fee for payment can have the unfortunate effect of obscuring the nature of the underlying economic transaction. For instance, people who join a gym often don’t realize that they’re paying for everything—the treadmill, the sauna, the swimming pool—regardless of whether they actually use it. They think the fee goes to the club, and the club buys the equipment (along with the services of those who work there). They don’t realize that the club is just an intermediary, and that it is really the members, collectively, who are doing the purchasing.

The second important point is that club purchasing often involves a significant reduction of consumer choice. When I go out to buy exercise equipment in the market, I pay for exactly what I want to use, and I don’t pay for anything else. When I join a club, the fee structure usually ensures that I have to pay for a share of everything, regardless of whether I use it. This is why people who like to swim usually get a better deal out of gym memberships than anyone else. Since the swimming pool is by far the most expensive item to maintain, there is almost always cross-subsidization among members of clubs that have a pool—an effect that clubs sometime seek to diminish by imposing a surcharge, such as a towel or locker fee, on those who use the pool.

This cross-subsidization among members is clearly one of the disadvantages of many club-purchased goods. It is partially attenuated by the fact that different clubs will arise that offer different mixes of goods, and so consumers can shop around for one that most closely caters to their preferences (for example, someone who doesn’t like to swim should not join a club with a pool). Although in theory one could get perfect efficiency here, in practice the amount of variety on display is fairly limited (as anyone who has compared fitness clubs can attest). This shows that the efficiency gains arising from the collective purchase (that is, the formation of an optimal sharing group) are sufficiently great that they outweigh the losses caused by the bundle of goods being less tailored to the needs of the individual consumer.

One can see a similar phenomenon in the case of condominiums. Each building offers its members a mix of “private” amenities (living unit, parking space) and “public” ones (elevators, security, heating). The latter are paid for through flat monthly condo fees, and are essentially available to everyone in the building “for free.” Again, each condominium offers a different bundle of public (or club) benefits, with options such as a swimming pool, garbage removal, even concierge service. In some cases, this is because the goods are relatively nonrival, and so can easily be enjoyed by all. In other cases, it’s because the goods are relatively nonexcludable, and so everyone must be forced to pay in order to avoid a collective action problem. (This is the case with the security guard at the entrance, whose presence automatically confers a benefit upon everyone in the building.)

—

Hopefully this all seems quite plausible as an account of how health clubs and condominiums are typically organized. Now suppose someone comes along and says, “How high should condo fees be?” or “How much should a gym membership cost?” The answer, of course, is that it depends. The only limit in principle is the amount that people are willing to pay. How much they are willing to pay will be determined entirely by how much they want to consume the type of goods that are best purchased collectively. If the members of a health club want a new sauna, or the residents of a condominium want expanded parking facilities, they should expect an increase in fees in order to finance these purchases.

Does it make sense, when shopping for a condominium, to find the building with the lowest possible fees? Again, it depends. Some people are not particularly interested in having a swimming pool in the building or timely repairs to the elevators, so they might be perfectly happy living in a building with rock-bottom fees. Other people, who happen to have more of a taste for the sort of goods that are best purchased collectively, will want to live in a building with higher fees and more amenities. What matters, in other words, is not the absolute level of fees, but rather the value that one gets for them.

This may seem crushingly obvious, and it usually is in the case of condominium fees. Unfortunately, when it comes to the subject of taxes, people tend to get all confused. In the same way that members of a club pay a fee for admission and then enjoy a certain range of goods “for free” once inside, as citizens of a country we all pay fees and then enjoy certain other goods “for free.” In the latter case, we call the fee a “tax,” but it has essentially the same structure as a club fee.

The fact that some goods are provided for by the state, financed through taxes, is a reflection of the optimal sharing group for those goods. In some cases, the optimal sharing group is everyone (consider national defense, the sewage and water system, highways). In this case, the good is provided by the “club of everyone,” which is to say, the state. The police are no different in principle from the security guard at the front desk of a condo. Furthermore, payment for these services—in the form of taxes—is mandatory for the same reason that condo fees are mandatory: The benefits are relatively nonexcludable (which is to say, unreasonably costly to exclude people from).

One of the goods that can often be purchased most efficiently through taxes is insurance. Since the benefits of an insurance scheme come from the pooling of risks, the size of the gain is often proportional to the size of the pool. As a result, it is in our interest in many cases to purchase insurance using the mechanism of universal taxation and public provision. This is basically how the health care system in Canada works. I pay taxes, and what I get in return is a basic health-insurance policy, provided by the state. So if Canadians want to consume more health care or a new subway or better roads, what are their options? The situation is the same as with the condo residents who want a new sauna: If people want to buy more of this stuff (and are willing to buy less of something else), then they should vote to raise taxes and buy more of it. It doesn’t necessarily impose a drag on the economy to raise taxes in this way, any more than it imposes a drag on the economy when the residents of a condo association vote to increase their condo fees.

One can see, then, the absurdity of the view that taxes are intrinsically bad, or that lower taxes are necessarily preferable to higher taxes. The absolute level of taxation is unimportant; what matters is how much individuals want to purchase through the public sector (the “club of everyone”), and how much value the government is able to deliver. This is why low-tax jurisdictions are not necessarily more “competitive” than high-tax jurisdictions (any more than low-fee condominiums are necessarily more attractive places to live than high-fee condominiums). Furthermore, the government does not “consume” the money collected in taxes—this is a fundamental fallacy; it is merely the vehicle through which we organize our spending. In this respect, taxation is basically a form of collective shopping. Needless to say, how much shopping we do collectively, and in what size of groups, is a matter of fundamental indifference from the standpoint of economic prosperity.

There is enormous confusion on this point. Every year, in dozens of countries around the world, right-wing anti-tax groups calculate and then solemnly declare a “Tax Freedom Day,” in order to let people know what day they “stop working for the government and start working for themselves.” But it would make just as much sense to declare an annual “mortgage freedom day,” in order to let homeowners know what day they “stop working for the bank and start working for themselves.” It takes the average homeowner at least a couple months of work each year to pay off his or her annual mortgage bill. But who cares? Homeowners are not really “working for the bank;” they’re merely financing their own consumption. After all, they’re the ones living in the house, not the bank manager. It’s the same thing with taxes. You’re not really “working for the government” when your kids are going to public school, you’re commuting on public roads, and you expect the government to pay your hospital bills when you’re old and infirm. You’re simply financing your own consumption.

One can find a similar fallacy at work in the widespread belief that tax cuts “stimulate” the economy. This is the same as believing that a legislated reduction in condo fees would stimulate the economy. Naturally, if condo fees go down across the board, it will result in people having more money in their pockets to spend. But it will also result in condo boards having less money to spend. The result will simply be a shift away from the sort of goods that are provided on a club basis toward the sort that are provided on a private basis. Tax cuts have the same effect. They just mean less money spent on schools and health care, more spent on cars and homes. Absent some effect on savings, the increased demand that occurs in one sector is necessarily offset by decreased demand in some other. (An exception to the rule occurs when the government has no money, and so has to borrow to make up the shortfall in tax revenue. In this case, the tax cut is not really a tax cut—it’s more like a mandatory personal consumption loan taken out by the state for each citizen. Either way, the same effect could be achieved by having the state spend the borrowed money on health care, pollution abatement, highway construction, or any other form of publicly organized consumption.)

There are, of course, certain costs associated with the use of the taxation system as a way of purchasing goods and services. For various reasons, taxes can’t be imposed as “flat fees” the way that club fees are usually imposed (Margaret Thatcher tried, in the U.K., but didn’t get very far with it). This means that they must be collected in other ways, such as income and consumption taxes, which distort economic incentives and generate all sorts of counterproductive tax-avoidance behavior (such as individuals hiring crafty accountants to discover and exploit tax loopholes). Yet this is not a phenomenon that is unique to taxation. Private markets also have transaction costs, such as exposure to the risk of fraud or the need to hire lawyers to look over contracts. That doesn’t mean that no one should hire a lawyer, and it doesn’t mean that no one should pay taxes. The underlying problem is that people behave non-cooperatively. As a result, we need to worry about being defrauded or taken advantage of in commercial transactions. We also need to worry about being assaulted and about having our property stolen. In order to decide what’s best, we have to weigh the benefits of the contemplated transaction against the costs of organizing it in a particular way. How much does it cost to hire a lawyer versus how much does it cost to get defrauded? How much does it cost to pay taxes (in terms of deadweight losses) versus how much does it cost to live with market failure?

The question, in other words, is simply whether the benefits that come from the formation of an optimal sharing group outweigh the costs that are associated with the particular sharing arrangements adopted. To say, as Milton Friedman once did, that any tax cut is a good tax cut is simply to articulate an arbitrary preference against a particular type of purchasing arrangement. It’s like saying that the best condo fee is the lowest condo fee. A lot of first-time buyers do have this attitude, but they usually come to regret it.

—

One of the things that tend to muddy the waters when it comes to understanding club goods is that we often give things different names when they are purchased collectively and when they are purchased individually. To take a somewhat exotic example, consider the case of the life annuity. This is basically an insurance product that people buy in order to protect themselves against the risk of outliving their savings. Although the precise details are usually complex, the basic idea is that one pays a flat sum up front in return for a fixed periodic payment starting at the age of retirement and continuing until death (for example, one might pay $1,000 now in return for a guaranteed payment of $10 a month from retirement until death).

Why might someone choose to buy an annuity? Statistics can tell us, on average, how long each of us can expect to live, and we can infer from this how much we will need to save for our retirements. But unfortunately, there is a fair degree of variation around this mean. As a result, we all face the risk of either saving too much or, more important, saving too little. For any one individual, it may not make sense to save enough to maintain a comfortable lifestyle until the age of 90, but the fact is, lots of people live that long. One solution, therefore, is to buy an annuity. If you die young, you don’t get much out of it, but if you live for a long time, it’s guaranteed to keep paying out. When an insurance company sells annuities to hundreds or thousands of customers, the ones who die young are likely to balance out those who live longer, so the total of payments made is likely to be quite close to what one could anticipate simply by looking at mortality tables and average life expectancy.

There is a problem, however, in the market for life annuities. It’s known as “adverse selection.” Basically, a life annuity is a good deal if you expect to live for a very long time, but a bad deal if you expect to die young. As a result, the only people with an incentive to buy them will be those who, for some reason or another, expect to live for longer than the average. In some cases, the reasons people have will be obvious. Women, for instance, typically have a life expectancy five years longer than men, so the value to them of a life annuity is significantly greater. As a result, any insurer that sets a “unisex” price for life annuities would tend to attract only female customers. This would in turn result in greater-than-expected liabilities.

Women, therefore, have to pay more for life annuities than men do (typically, the same up-front payment purchases a lower periodic payment). Yet there are many other factors affecting life expectancy that are not so easily detectable by insurance companies (for example, whether or not you smoked when you were young). As a result, insurers tend to attract precisely the sort of customers that they least want. In effect, the mere fact that a person is interested in buying a life annuity is cause for suspicion, since it suggests that he expects to live for a long time. This “adverse selection” effect needs to be taken into consideration when setting the price of the annuities. But because of this, many of the “good risks”—people who are likely to die young—will be priced out of the market, since they cannot credibly identify themselves to the insurer as good risks. Annuities will simply be too expensive for it to be worth their while to purchase them.

This problem is somewhat attenuated, however, if people go shopping for annuities as a group. For example, if an employer approaches an insurance company and says, “I’d like to buy life annuities for all my employees,” this is inherently less suspicious. After all, since very few companies make employment decisions based upon anticipated longevity, a company’s employees are likely to be a fairly representative sample of the population (for each one who lives a very long time, there is likely to be one who dies young). The insurer can therefore sell life annuities to the group at a better rate than it can to individuals. A life annuity is thus the type of good that has an optimal sharing group larger than one: It is best purchased not as a private good, but as a club good.

Unfortunately, when we purchase life annuities as a group through an employer, they are no longer called annuities. Instead, they are called “defined benefit pension schemes.” This change in nomenclature creates all sorts of confusion; there is an inclination to regard pension schemes as savings arrangements, rather than as insurance products. Nevertheless, an annuity is essentially what is being purchased: In return for an up-front payment (the “pension contribution”), the employer guarantees a fixed periodic payment from the time of retirement until death.

Of course, if it pays to shop for annuities as a group, then the bigger the group, the better. The benefit, in this case, comes from belonging to a group that can credibly claim to be a representative sample of the population. And of course, the best sample of the population is the population itself. As a result, the optimal sharing group for life annuities is the entire country. No surprise then that the state also “purchases” life annuities for its citizens, in the form of public pensions (the Canada Pension Plan, Social Security in the United States).

The failure to appreciate that what is being provided here is a life annuity creates considerable confusion. In the debates over “privatization” of Social Security in the United States, for instance, people routinely compared the rate of return of money that was saved and invested in the stock market with the rate of return of money paid into Social Security. Yet analyzing the latter in terms of rate of return involved a category error. It amounted to comparing an investment to an insurance policy. In this respect, it is like calculating the rate of return on your car insurance: If you had no accidents, your rate of return looks terrible; if you crashed your new Mercedes in the first month of your policy, the rate of return looks great. The same is true with Social Security: If you live until you’re 120, the rate of return is going to be spectacular. But that misses the point. People buy insurance not because they hope to get a payout, but because of the peace of mind that comes from being protected against particular risks. With state pension plans and other annuity products, knowing that you can’t outlive your savings serves as the primary source of benefit (among other things, it relieves people of the need to have so many children).

Thus what proponents of “privatization” of Social Security in the United States were recommending was not really privatization of the system. Privatization would involve individuals purchasing life annuities privately, rather than collectively—which would be a transparently bad deal. What they were actually recommending was that individuals stop purchasing insurance entirely, and instead simply save for their own retirements. (Many proponents of “defined contribution” over “defined benefit” pension plans are making the same recommendation.) In other words, their goal was simply to undo a mutually beneficial risk-pooling arrangement, for no particularly good reason other than an ideological hostility to government. No wonder the idea didn’t go anywhere.

—

There is, of course, one big difference between paying fees to a club and paying taxes to the government. It is an almost inevitable consequence of shared consumption that it reduces consumer choice. No condominium is likely to provide exactly the mix of “public” amenities that you most value. No health club is likely to have exactly the equipment that you would have bought for yourself. And yet with clubs the consumer still has some choice. Not only can you shop around to find the one that is the best fit, you also have the option of leaving, if, say, decisions get made that are too far contrary to your desires. People may hate condo and gym membership fees, but they are not forced to pay them.

In the case of the state, however, this exit option is typically absent (even if you do leave, you may not find any other state willing to take you). Thus the mix of goods you get by virtue of membership is likely to be crudely mismatched to your needs (“Public schools—what do I need those for? I have no kids …”). The provision of public goods by the state is not just a case of collective shopping; it is also a case of compulsory collective shopping. So while the economic character of the transaction may be the same in the two cases, in the case of the state there is an interference with individual liberty that is felt by many to be a rather keen insult.

What is to be said here? Of course, the observation is correct. You have to pay your taxes, and you have to pay for a wide variety of public goods even if you don’t use them. Because of this, state provision should be considered only in cases of egregious market failure, when a one-size-fits-all provision is better than the alternative. This is why the state is often more successful in dealing with relatively homogenous goods, such as insurance, where differences in consumer preference are not all that significant. (Compare this to food or clothing, where the advantages of being able to shop around are obviously much greater.) A more general way of putting it would be to say that the optimal sharing group will tend to be larger for goods where consumer preference is more homogeneous, because the losses caused by “preference mismatch” will tend to be smaller.

All that having been said, it is important to note that the amount of uniformity in the package of benefits offered by government is often overstated. This is particularly true in federal states, where the major functions of the welfare state are often discharged at a more local level and where there are very few internal barriers to mobility. Like different health clubs offering a different mix of fitness equipment, each U.S. state or Canadian province offers a different mix of club goods. If you want subsidized daycare, move to Quebec, not Alberta. If you want state-funded universities, move to California, not South Carolina.

Even in a nonfederal system, every country delivers a large number of public services at the level of the municipality, and municipalities compete with one another for both people and businesses by trying to offer an attractive mix of taxation and public services. If you’re willing to make certain idealizing assumptions about geography and mobility, the economist Charles Tiebout has shown that municipal governments are able to achieve the same level of efficiency as private markets. Of course, this all needs to be taken with a grain of salt. What it shows, however, is that people who argue for the superiority of private over public provision on the grounds of choice often overstate the amount of choice that actually exists in private markets, while understating the amount of choice that exists in the public sector.

It is worth observing as well that in most cases, when the welfare state provides a certain good, it does so at a very low level, leaving consumers free to “top up” their entitlements by purchasing more of the good on private markets. This is true in all the major categories of welfare-state expenditure: pensions, education, security, disability insurance, health insurance, communications (such as postal services), and sometimes even transportation networks. Thus it is the poor who suffer most acutely from restrictions on consumer choice—but they are not likely to complain, since the one-size-fits-all package that they receive is of much greater value than anything they would have been able to afford on their own.

Finally, it is important to distinguish those who want to exercise an exit option from those who simply want a free ride. In the case of a gym membership, you are always free to quit if you don’t think you’re getting your money’s worth. But the gym also has the right to kick you out—to exclude you from its benefits—if it doesn’t like the way you are behaving. States, on the other hand, cannot kick people out (barring certain exceptional cases). The state health care provider cannot discontinue your policy after you develop diabetes, the way a private insurer can. There is an obvious quid pro quo here: a limited right of exit is coupled with a limited right of exclusion. The latter provides a benefit—in the form of peace of mind—that is often taken for granted.

In the face of all these points favoring public insurance, conservatives will sometimes fall back on the argument that giving everyone insurance coverage, whether it be insurance against poor health or old age or whatever else, is irresponsible because it encourages people to engage in riskier or more careless behavior – the so-called problem of moral hazard. As Taylor explains it:

Moral hazard […] means that having insurance leads people to take fewer steps to avoid or prevent the bad event from happening in the first place. The insured have a little bit less incentive to change the habits or improve the conditions that make them more vulnerable to a negative event. For example, a company with good fire insurance might worry less about preventing fires at an older factory. Someone with insurance against theft might be less likely to buy a security system. Someone with health insurance is more likely to head for the doctor for every sniffle and cough than someone without health insurance. As a result of this disincentive, the existence of insurance makes the payouts from insurance higher than they would otherwise be.

This is a legitimate concern, and one that any public insurance plan has to account for. As Heath points out, though, it’s also one that any private insurance plan has to account for, because it’s an issue inherent to insurance in general, not just to government-sponsored insurance; so it doesn’t really make sense to use it as an argument against public insurance unless you’re also arguing against the whole concept of insurance itself, in every form:

[There is a] fallacy underlying the “personal responsibility” crusade of the right. Conservatives blame government handouts for undermining the spirit of self-reliance. This is just a moralizing way of describing a generic problem with insurance systems, where indemnity (“handouts”) tends to generate moral hazard (“irresponsibility”). What conservatives fail to realize is that the moral hazard effect in question is a generic feature of any type of insurance system—it has nothing to do with the question of public or private ownership. There is, however, a prior selection effect that gets ignored. Because private insurance markets are so prone to failure in the face of information asymmetries, the type of insurance that is usually prone to moral hazard or adverse selection tends to be feasible only when provided by the “the insurer of last resort”: the state. So it doesn’t make much sense to blame government for the moral hazard. It’s usually because of the moral hazard problem that the government is running the program in the first place.

When criticizing various aspects of the “social safety net,” conservatives chronically make the error of drawing an invidious comparison between the moral hazard effects of government insurance and the moral hazards effects of no insurance at all. It’s no surprise that the latter wins. This is a clear instance of the “add up the costs, ignore the benefits” fallacy. Having no insurance means you don’t have to suffer the losses caused by moral hazard, but it also means that you have to suffer the losses of having no insurance. Naturally, self-insurance has lower costs; the problem is that it also has no benefits. Thus the only way to make it look good is to consider only the costs and to disregard the forgone benefits.

Unfortunately, the no-insurance option is routinely described in public debate as “privatization,” not as “abolition” of the insurance scheme. For it to be real privatization, the comparison would have to be between government provision and private provision of the same type of insurance. Privatizing Social Security, for instance, would mean sending individuals out to buy their own life annuities on the open market, not having them invest in mutual funds. When the comparison is constructed in this way, government provision often comes out looking quite good.

Consider the case of health care. American critics of “socialized” medicine often regard it as a synthetic a priori truth that public provision will generate overconsumption, followed by rationing of care. “If you think health care is expensive now,” they say, “wait until you see how much it costs when it’s free.” If the government started giving away free cheese, people would start eating too much cheese. So why would anyone want to give away free health care?

This line of reasoning, however, contains two obvious errors. First of all, socialized medicine on the single-payer model doesn’t mean socialized health care, it means socialized health insurance. In Canada, for example, health care provision is almost entirely private. (I can assure you, since my wife is a surgeon. Not only is she privately incorporated, I am happy to report that her corporation is quite profitable.) Obviously, the fact that health insurance is provided to all citizens “for free” does not generate overconsumption of insurance, since it’s provided in the form of a standard, universal benefit. Second, except in the most unusual of cases, Americans don’t pay for health care out of pocket. They also participate in various risk-pooling arrangements, ranging from private insurance and health management organizations to government-supplied Medicare and Medicaid. Thus the typical health care consumer faces exactly the same incentives at the front end in Canada and the United States. Health care is all “free” at the point of purchase.

Thus the conservative critique of socialized medicine is not actually a critique of public ownership and provision. It is a critique of health insurance in general, both public and private. One can see this in the remedy that conservatives offer for the problems of moral hazard in the health insurance system, namely, health savings accounts. These sorts of proposals are usually based on the assumption that the reason for government involvement in the health care sector is that not everyone can afford it. (This is already a mistake, since the rationale for public health insurance is not distributive justice, but rather market failure. It is only the non-actuarial structure of the premiums in social insurance schemes that is motivated by considerations of distributive justice.) Thus the proposed solution is to give each individual citizen a yearly grant, to be kept in a special savings account. The individual would save or spend this money on health care, as needed. Because individuals would start paying for health care out of pocket, the argument goes, they would lose whatever incentive they may have to overspend.

The problem with these proposals is that they are grotesquely inefficient. Health care spending in our society generally follows what’s known as the 80/20 rule: 20% of the population is responsible for roughly 80% of the health care spending. Thus the figure of $2 trillion in annual health care spending in the United States, or $6,700 per person, is slightly misleading. A better aggregate picture would be to imagine one person spending $26,800 per year, along with four others spending only $1,675. So what happens if the government gives everyone $6,700 in a special little account? How much should you save? Well, I guess that depends on whether or not you intend to develop diabetes … But of course, you don’t know if you are going to get diabetes, just as most other people don’t know what their future health care needs are going to be. Furthermore, since spending is going to be highly uneven across the population, giving everyone a grant of the same size guarantees that the state will give too much to most people and not enough to virtually everyone who is really going to need it.

But across large population groups, health care spending (not to mention rates of disease) is highly predictable. This means that there is an overwhelming efficiency argument to be made for the pooling of health care savings. This also means that, when you examine any of the more mainstream proposals for health savings accounts, their bark tends to be much worse than their bite. Recognizing that the only rational way to organize the bulk of health care spending is through insurance, what conservatives typically propose is a set of relatively small grants at the front end (perhaps $2,000) coupled with a “catastrophic coverage” insurance mechanism at the back end. When all is said and done, the savings account winds up being just a heavy-handed way of discouraging parents from bringing little Johnny to the emergency room every time he gets the sniffles. It’s the back-end insurance mechanism that does all the heavy lifting, covering the cost of all major procedures and accounting for the bulk of health care spending. The same policy objectives could be achieved within a socialized medicine system simply by imposing a small user fee on hospital visits (as they do in Sweden), or in a regular private insurance system by having a large deductible.

So where does all this leave the issue of personal responsibility? Conservatives are not wrong to think that there is a fundamental tension between the old-fashioned ideals of individual liberty, responsibility, and self-reliance and the practices of what European intellectuals like to call the “risk society.” Yet they blame the decline of personal responsibility on government, whereas what they should be blaming is the rise of insurance. As François Ewald (perhaps the most original French thinker on the subject of the welfare state) argues, the decisive rupture with the old-fashioned ideal of personal responsibility occurred in the nineteenth century, with the development of actuarial science and the rise of the private insurance industry. Government in the twentieth century, in developing the social safety net, was simply borrowing techniques that had been developed in the private sector. “Personal responsibility” was dead long before they got to it.

Whether or not one regards this as a good thing overall, it’s important to keep in mind that the development of comprehensive insurance systems coincides with the emergence of capitalism as a relatively stable economic system. Insurance does a lot more than simply keep the taxis on the street in Hong Kong. Every single aspect of our financial and commercial system, every transaction that we engage in, is underwritten at some level by insurance. It truly is the all-purpose economic lubricant. Unfortunately, it also requires us to be somewhat less fastidious when it comes to holding people responsible for their actions. But what can you do? Welcome to the modern world.

For the sake of discussion, we can ask what might happen if we did simply abolish all these forms of social insurance and just left it to individuals to bear full financial responsibility for their own healthcare and their own retirement and so on, without engaging in any kind of collective risk-pooling. But the clear answer, in short, is that it wouldn’t go well. As Pinker explains, human nature just isn’t built to perfectly optimize for our long term interests as individuals in every instance – even when we have resources to spare (which not all of us do), we’re often bad at saving them – so in order to keep ourselves on track, it can make sense for us to put matters in the hands of some separate entity (like government) which can handle a portion of the long-term planning and saving on our behalf:

An important challenge to conservative political theory has come from behavioral economists such as Richard Thaler and George Akerlof, who were influenced by the evolutionary cognitive psychology of Herbert Simon, Amos Tversky, Daniel Kahneman, Gerd Gigerenzer, and Paul Slovic. These psychologists have argued that human thinking and decision making are biological adaptations rather than engines of pure rationality. These mental systems work with limited amounts of information, have to reach decisions in a finite amount of time, and ultimately serve evolutionary goals such as status and security. Conservatives have always invoked limitations on human reason to rein in the pretense that we can understand social behavior well enough to redesign society. But those limitations also undermine the assumption of rational self-interest that underlies classical economics and secular conservatism. Ever since Adam Smith, classical economists have argued that in the absence of outside interference, individuals making decisions in their own interests will do what is best for themselves and for society. But if people do not always calculate what is best for themselves, they might be better off with the taxes and regulations that classical economists find so perverse.

For example, rational agents informed by interest rates and their life expectancies should save the optimal proportion of their wages for comfort in their old age. Social security and mandatory savings plans should be unnecessary—indeed, harmful—because they take away choice and hence the opportunity to find the best balance between consuming now and saving for the future. But economists repeatedly find that people spend their money like drunken sailors. They act as if they think they will die in a few years, or as if the future is completely unpredictable, which may be closer to the reality of our evolutionary ancestors than it is to life today. If so, then allowing people to manage their own savings (for example, letting them keep their entire paycheck and investing it as they please) may work against their interests. Like Odysseus approaching the island of the Sirens, people might rationally agree to let their employer or the government tie them to the mast of forced savings.

The economist Robert Frank has appealed to the evolutionary psychology of status to point out other shortcomings of the rational-actor theory and, by extension, laissez-faire economics. Rational actors should eschew not only forced retirement savings but other policies that ostensibly protect them, such as mandatory health benefits, workplace safety regulations, unemployment insurance, and union dues. All of these cost money that would otherwise go into their paychecks, and workers could decide for themselves whether to take a pay cut to work for a company with the most paternalistic policies or go for the biggest salary and take higher risks on the job. Companies, in their competition for the best employees, should find the balance demanded by the employees they want.

The rub, Frank points out, is that people are endowed with a craving for status. Their first impulse is to spend money in ways that put themselves ahead of the Joneses (houses, cars, clothing, prestigious educations), rather than in ways that only they know about (health care, job safety, retirement savings). Unfortunately, status is a zero-sum game, so when everyone has more money to spend on cars and houses, the houses and cars get bigger but people are no happier than they were before. Like hockey players who agree to wear helmets only if a rule forces their opponents to wear them too, people might agree to regulations that force everyone to pay for hidden benefits like health care that make them happier in the long run, even if the regulations come at the expense of disposable income. For the same reason, Frank argues, we would be better off if we implemented a steeply graduated tax on consumption, replacing the current graduated tax on income. A consumption tax would damp down the futile arms race for ever more lavish cars, houses, and watches and compensate people with resources that provably increase happiness, such as leisure time, safer streets, and more pleasant commuting and working conditions.

Whether or not such a consumption tax would be exactly the right mechanism for this kind of reallocation of resources is, of course, debatable (see our whole long discussion earlier on the pros and cons of different kinds of taxes). But however the necessary funds might be collected, what seems clear is that it’s possible for us to improve our society as a whole by using our power of collective action to overcome some of our less-than-perfectly-optimal tendencies as individuals. We may not be able to change our own nature, but with a bit of ingenuity, we can create institutions that help offset some of the undesirable side effects of our occasional irrationality. Some traditional conservative economists might want to deny that the propensity for such irrationality is even a part of our nature at all, and that there’s therefore nothing to fix – but as Alexander points out, the facts seem to indicate otherwise; so the best thing we can do for ourselves, if we want to maximize our own interests, is to set up our society in a way that’s capable of recognizing and correcting for those tendencies:

[Q]: What do you mean by “irrational choices”?

A company (Thaler, 2007, download study as .pdf) gives its employees the opportunity to sign up for a pension plan. They contribute a small amount of money each month, and the company will also contribute some money, and overall it ends up as a really good deal for the employees and gives them an excellent retirement fund. Only a small minority of the employees sign up.

The libertarian would answer that this is fine. Although some outsider might condescendingly declare it “a really good deal”, the employees are the most likely to understand their own unique financial situation. They may have a better pension plan somewhere else, or mistrust the company’s promises, or expect not to need much money in their own age. For some outsider to declare that they are wrong to avoid the pension plan, or worse to try to force them into it for their own good, would be the worst sort of arrogant paternalism, and an attack on the employees’ dignity as rational beings.

Then the company switches tactics. It automatically signs the employees up for the pension plan, but offers them the option to opt out. This time, only a small minority of the employees opt out.

That makes it very hard to spin the first condition as the employees rationally preferring not to participate in the pension plan, since the second condition reveals the opposite preference. It looks more like they just didn’t have the mental energy to think about it or go through the trouble of signing up. And in the latter condition, they didn’t have the mental energy to think about it or go through the trouble of opting out.